Your author has been listening to podcasts while helping TM TKO prepare some exciting new features (hopefully out really soon! more here shortly), especially Mike Duncan’s History of Rome.

Inspired – for better or worse – I did some research on how frequently marks containing famous Roman figures pop up on various trademark registries. I limited the search to the more prominent kings, consuls, and early emperors of Rome, so this isn’t close to an attempt to find a full cultural footprint. I definitely haven’t taken into account any language equivalents, either, so this is probably both over-and-under-inclusive in non-primarily-English jurisdictions.

Jurisdiction

Active Count

USA

694

Canada

183

Mexico

705

EU

658

France

392

Germany

353

Spain

531

UK

768

Australia

185

New Zealand

52

Reflected Roman glory

The sheer range of products and services to which these ancient, still somewhat-known names have been applied is amusing in its incongruity. A few fun ones, selected at random:

SULLA for bath towels? Sure! Who wouldn’t want the same sort of fluffy comfort that the dictator may have used to dry off the blood of Jugurtha, the Cimbri, the Socii, the Athenians, or, oh, the Romans?

How about TIBERIUS for cigars? After all, why not get your nicotine from the “gloomiest of men“?

ROMULUS for a variety of guns and weapons does seem pretty on-point, though; it’s hard to murder your brother, rape the Sabines, and endlessly war with your neighbors without some armaments.

Sadly, there are no filings for GRACCHUS or GRACCHI for any agricultural products or services, or property reallocation services, but there is a WIPO-based registration for pharmaceuticals and beverages. Perhaps you can talk a client into adopting a mark inspired by these under-commercialized historical demagogues.

The USPTO’s recent show cause order to Chinese IP firm Shenzhen Huanyee Intellectual Property Co., Ltd., about its alleged unauthorized practice of law in the US in over 8,000 applications and widespread use of false information in those applications. The Office may invalidate all such applications.

The USPTO has issued these in other situations, like this 2018 order to USAEU Intellectual Property Agency Co. Ltd. (over 2,500 applications) and a prior round of 2016 enforcement. Prior rounds of enforcement did not invalidate the applications or resulting registrations, so the Office is definitely being more aggressive this time. A list of enforcement actions — lots of which are against Chinese representatives — is available here.

TM TKO did some research on some of the most common Chinese email providers (qq.com, 126.com, 163.com, sina.com, 139.com, sohu.com, and foxmail.com) and how frequently email addresses from those providers are used as the correspondent of record in USPTO trademark filings. It’s a lot! A surprisingly large number of these just flatly list a firm with a Chinese address as correspondent — at least 50%. This isn’t necessarily problematic — a US-licensed attorney could be practicing there — but I wouldn’t be shocked to find future unauthorized practice actions against some counsel of record in this data set.

2021: 23,500+

2020: 49,000+

2019: 22,300+

2018: 22,200+

2017: 22,900+

2016: 14,600+

The number of applicants listing a US address and using a typically-Chinese email address is pretty high. Again, it’s not impossible that this happens, but I’d be shocked if a decent percentage of these (a) don’t have a common “address” and (b) wouldn’t be of some interest to the PTO’s disciplinary czars.

2021: 540+

2020: 1800+

2019: 640+

We’ll be monitoring additional USPTO enforcement actions to see if this aggressive enforcement comes to pass (especially invalidating applications) turns into a continuing priority, or is more of a sporadic twitch of their enforcement muscles.

It’s a beautiful spring so far, and we’re all enjoying the pretty blossoms and the pollen-driven sneezes that go along with getting outdoors. To honor the return of all the grasses, trees, and other plants in our lives, we’re taking a closer look at how trademarks interact with these products.

There is a big exception — the “varietal” or “cultivar” names of a cultivated variety of subspecies of a plant or seed. The Office considers these to be the equivalent of the “generic” name for the plant or seed, regardless of whether the name is a fanciful name or a code. TMEP § 1202.12. The varietal or cultivar name is used in a plant patent as the identifier for the variety of plant or seed, and remains so regardless of whether the patent expires. In re Pennington Seed Co., 466 F.3d 1053, 80 USPQ2d 1758, 1762 (Fed. Cir. 2006).

More arbitrary names are another matter altogether. Companies often pick a name for the new product without taking trademark concerns into account, and attempt to protect the cultivar name as a trademark. This never goes well.

The Office views these as incapable of functioning as a trademark – the equivalent of an insurmountable genericness refusal. No amount of advertising expenditure can salvage it as a mark. See, e.g., In re Farmer Seed & Nursery Co., 137 USPQ 231, 231-32 (TTAB 1963). It doesn’t even matter if the varietal name was never actually used — it’s sufficient that it was registered as a varietal name. In re American Onion Int’l, Inc., Ser. No. 76660662, p. 5 (TTAB Aug. 8, 2008), available at https://ttabvue.uspto.gov/ttabvue/v?pno=76660662&pty=EXA&eno=13. However, if a term is a variety name for one type of plant (like a dianthus) it won’t bar registration of that term for a different plant (like an apple tree), at least if the applicant makes that clear in their description of goods. See, e.g., the registration for RED ROMANCE, Reg. No. 5493245.

The University of Minnesota, which developed the varietal, attempted to register HONEYCRISP for “apple trees, namely variety Minnesota 1711 R.” Ser. No. 74156209. The Office’s online records are spotty in the early 1990s, and the full file history is not online, but it went abandoned due to a failure to respond to an Office Action — we can confidently assume that it foundered on the plant varietal refusal. In other applications, the Office also found the term descriptive or generic as applied to related goods, like cider.

Plant varietal refusals don’t often make it to the TTAB. But, a prominent recent example saw Rainier Fruit Company’s attempt to register a lightly stylized version of HONEYCRISP for apples. Rainier didn’t even try to argue the cultivar issue — it disclaimed HONEYCRISP — but the stylization was not sufficiently distinctive.

What’s getting through? Marks that pair HONEYCRISP with an additional, (more) distinctive elements. The two currently active registrations are a Supplemental Registration for PREMIER HONEYCRISP, with HONEYCRISP disclaimed, for “live honeycrisp apple trees,” and a Principal Register registration for ROYAL RED HONEYCRISP for “live apple trees.”

Takeaways for Trademark Lawyers

Please make sure your clients plan for trademark protection before filing for a plant varietal production certificate and plant patents. If trademark and patent counsel are not on the same page, using the cultivar name in the PVP certificate will be fatal to attempts to claim trademark rights in that term.

This is going to end up a very short post, even if the research ended up taking a while! We decided to compare the extent to which Major League Baseball and the Premier League teams protected their IP, comparing US filings for the Premier League teams and EUIPO filings for the baseball teams.

Baseball had pretty comprehensive filings for key marks in the EUIPO in Classes 25 (clothing merch) and 41 (games / etc.). The top of the Prem’s financial tables had similar coverage, but the bottom — newly promoted or up-and-down teams like Leeds, Burnley, Fulham, West Brom, and Sheffield United — had no US coverage; Aston Villa had a registration in Class 25 but not 41. Even an upper-middle-class team, by both the table and revenues, Everton, had no US filings for its house mark.

What accounts for this difference? It may be due to organizational differences. While MLB teams own their own marks domestically, MLB registers marks on its teams’ behalf internationally. Teams in the Prem appear to on their own — and a less-popular team may view international coverage as a great investment if they just don’t have much of a fan base outside of their local market. Among the US major sports, baseball and hockey are generally thought of as having more local fan bases than the nationally-driven interest in the NBA and NFL, but they haven’t stinted on their European brand protection efforts.

The Difficulties Facing the US Patent & Trademark Office in Examining Specimens

The trademark community has been mildly frustrated with the Trademark Office in 2020 and into 2021 for two related reasons:

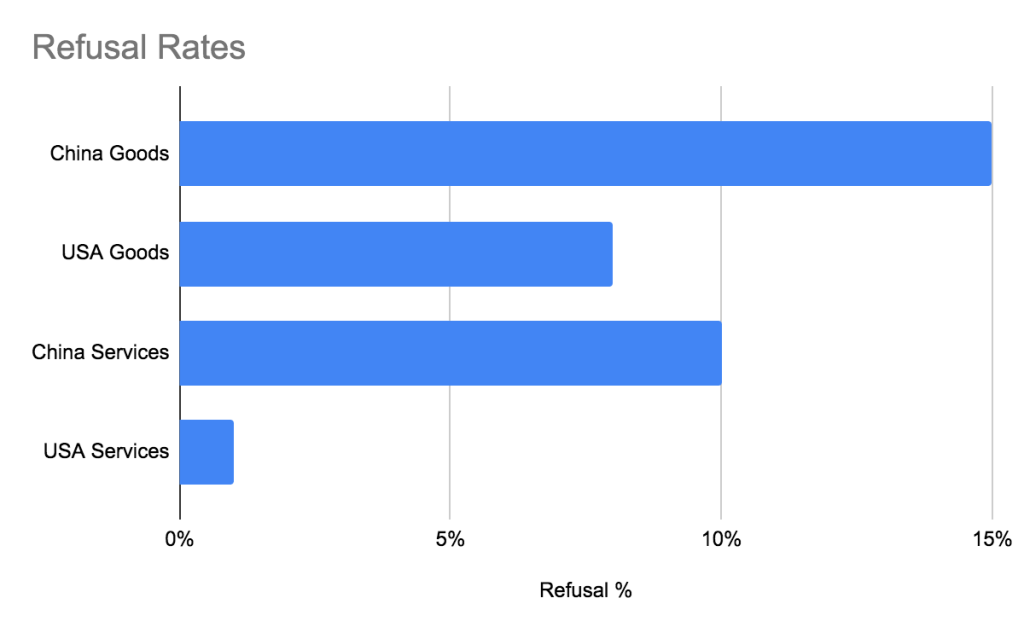

the feeling that a lot of crap has gotten onto the trademark registry, largely weird marks originating from China. Many of these are alleged to have dubious specimens or other issues with use claims, e.g. claiming use on a broad swathe of goods.

the feeling that otherwise perfectly valid specimens are getting caught up needlessly by new examination standards, increasing prosecution times and costs.

Let’s look at this from the Trademark Office’s perspective, and take a look at some examples of the sorts of applications that tend to generate practitioner discontent.

I. Spot-Checking New Applications For Specimen Issues

I focused on 1-word, use-based US filings without design elements filed by Chinese applicants in December 2020. I further restricted to just those that have the text “no meaning” to avoid translation/transliterations. The types of marks this generates – TERIQO, BEIYEIDEI, FABSMURD, MIZILI, URCHESE, FEOICH, and GOMNOA, are the sort of marks that tend to generate a skeptical eyebrow raise from practitioners. It’s a little ironic that these marks that generate practitioner skepticism are the most inherently distinctive marks on the protectability spectrum, since they’re gibberish in the first place.

I’m not sure; it’s a screenshot and invoice from SellersGlobal. The photo of the hand actually holding the tweezers is the easiest to see, and looks legit. The shipping address on the invoice is partially redacted, but seems to be missing an actual street address anyway.

From an online receipt shipping to the US. Receipts are a bit weird, since it should be the customer getting the receipt not the intermediary vendor (CoolMall), but it does at least seem to show shipping to the US.

Amazon sales pages for candles. Candles and fuel usually aren’t provided under the same mark, so the scope of the goods covered in the use claim seem more debatable than the specimen itself.

None of these seem to be clear problems taken on their own merits. But, what about in the aggregate?

II. The Broader Question — What Kind of Registry Do We Want?

There were 32,986 applications that met these narrow criteria in just December 2020. That’s a TON of applications. For comparison, in December 2015, there were 30,098 US applications filed in total. That’s 2,000 less than just this this subset of China-based 1(a), 1-word, not-a-translation, standard character marks applications!

Let’s assume that many of these sales/shipments are pretty low-volume, at least at the time of registration. What could be done to preserve a smaller registry that reflect the marks that US consumers are actually likely to encounter? One option might be to require a certain volume of commercial activity. This could avoid the issue of sellers obtaining registrations for de miminis sales through online platforms that aren’t very big in the US. This would obviously have some serious impacts, cutting off registration as an option for new ventures, or at least pushing more small businesses to “sit on” an ITU application while building up their commercial presence. It would also raise difficulties for non-commercial brands that don’t generate sales. Some of these could be addressed by evidence other than sales, like website visits from US IP addresses or the like (potentially game-able, but more work), or just by having different use standards for domestic and foreign applicants (though that may raise equal protection issues).

We certainly don’t have a perfect solution — we’d love to hear your thoughts as the Office continues to grapple with these examination complexities.

In July 2019, we took a look at “digitally altered” specimen refusals from the PTO. At the time, the Office had only just published its formal guidance on this new issue. In those early days, Chinese applicants were getting plenty of refusals, but generally overcame them pretty well.

This blog post does a deeper dive to see how often Chinese applicants are getting and faring with this refusal, and how those rates compare to US-based applicants. This only looks at the “digitally altered” refusal, not related issues with website specimen inadequacies like insufficient date / URL information. The “digitally altered” refusal is a “tougher” refusal — the Examiner is saying “this looks fake” rather than just “you forgot to include some key details.”

I. How Common are “Digitally Altered” Refusals?

We looked at applications that had digitally altered specimen refusals issued in 2020, broken down goods-classes vs. service-classes refusals. The final counts of the still-pending applications are considerable; whether these end up moving through to registration or going abandoned will make a big difference in assessing the impact of this examination priority. These counts looked at the refusal ratio as a percentage of the overall applications that had use claims at some point in the application; obviously, 1(b) or 44(e)-only or 66(a) applications won’t get this refusal.

Overall, currently or formerly use-based applications in the goods classes are getting a ton more “digitally altered” specimen refusals than specimen-class applications. That makes sense; most service-class specimens are websites anyway, and it’s just as easy to put up a crummy real website that will pass examination muster as it is to mock up a crummy fake website. Refusals of US applications with Chinese applicants were about twice as high as the rate of refusals of applications owned by US-based applicants for goods-based applications (15% vs. 8%) and about 10 times as high for services-based applications (10% vs. 1%). Because use-based applications in the goods classes from Chinese-based applicants actually outnumber such applications from US-based applicants since July 2019, when the USPTO announced this new prosecution focus, this means that almost twice as many these “digitally altered” refusals (by raw number counts) have gone out on applications where the applicant is based in China than to applications where the applicant is based in the US.

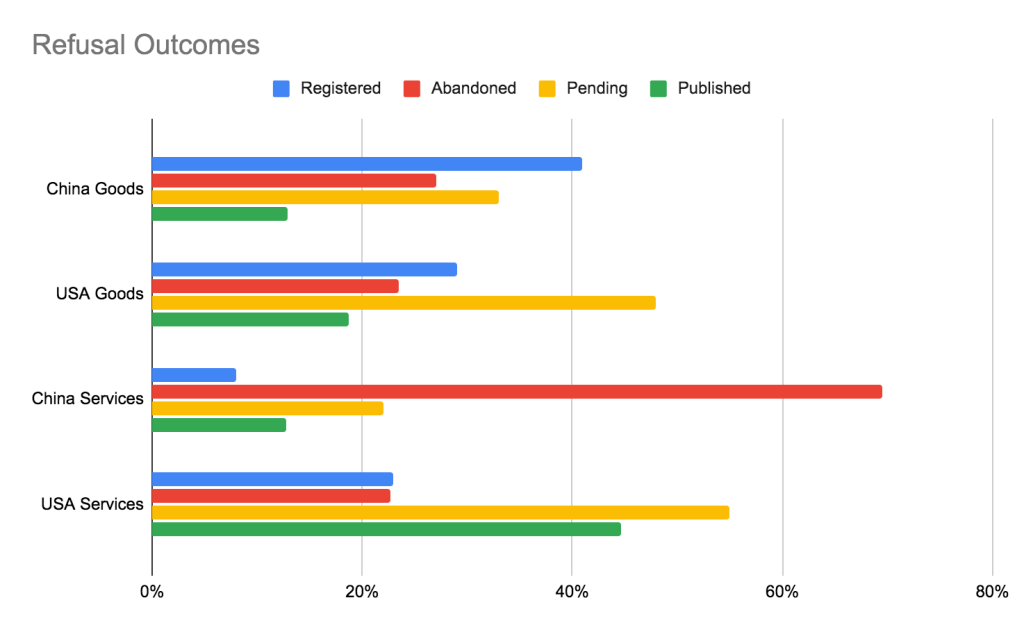

II. What Happens After Refusals?

So, what happens once these refusals are issued? A pretty good percentage of the applications that get those refusals are still pending – about 40% of applications from China-based applicants, and about 50% applications from US-based applicants. Of the rest, more applications are “fixing” the issue and getting through to registration, including a slightly higher percentage for China-based applicants overall (though very few of the smaller service-class dataset) than for US-based applicants.

III. Impact of the Rule

So, what is the impact of this rule? It has resulted in the abandonment of almost 6,200 applications from China-based applicants and almost 3,000 applications from US-based applicants. The sheer number of applications going abandoned that would have otherwise moved through to registration with a probably-fake specimen of use is a win for the goal of having a good, clean registry.

Does the rule occasionally impact “good-faith” applicants? Sure! It may cause a bit of inconvenience for a “legitimate” applicant where the goods are shown in a “glamour shots” on a pristine white background, US counsel can help train their clients to provide an appropriate specimen from the outset or in response to the Office Action.

IV. What Else Can Be Done?

Is this sufficient? Hell, no. There are plenty of sketchy specimens (from applicants of all nationalities!) that never generate a refusal, suspicious applications for a random assortment of letters for a list of goods that is very close to a class header, an epidemic of “use claims” that are far more broad than could ever be justified, and a raft of Section 8 and Section 71 claims that are way to broad and get trimmed sharply back every time the USPTO conducts a use claim audit (we blogged about audits in February). I’d love to see aggressive examination of broad use claims and specimens, even if it puts a greater burden on applicants and their counsel. I also believe that a change in the law to allow registrations under 44(e) or 66(a) to be trimmed back to reflect marketplace use essentially immediately after registration, putting them back on more even footing with US applications that claim use for goods or services where there is none, would be a net benefit and give us a cleaner registry. In fact, I’d love to see consequences from over-broad use claims beyond just deletion of the goods that are not in use.

Even if it’s not nearly enough, the digitally altered specimen rule has helped give trademark owners, applicants, and counsel a somewhat cleaner registry that more accurately reflects the real world of US commerce, and that’s a good thing.

Everyone loves a holiday, but, sometimes, work just can’t wait. In honor of our recently-passed Thanksgiving, we took a look at the trademark professionals who are clocking in while everyone else is taking off.

To do this, we looked at three data points: the number of new applications filed, the number of outgoing Office Actions (including requests for reconsideration, etc.), and the number of incoming Office Action Responses (same) to give us a look at both activity by the USPTO and by outside lawyers/the public.

Overall, activity has gone up by quite a lot over time: activity was basically nil in 1990 and 2000, and has risen markedly since 2010.

In 2000, there were only 32 applications with a filing date of Thanksgiving, 0 on Christmas, and two on New Year’s, opposed to an average of 780 per day. By 2019, there were 439 new apps on Thanksgiving, 300 on Christmas, and 223 on New Year’s, versus an average day of 1,355 — a substantial increase.

On the Office Action front, the USPTO has become increasingly active on the holidays, although there is some variability. Christmas 2010 saw a high-water mark of 244 outgoing Office Actions (but Christmas was quieter at 123), 2019 saw 105 on Thanksgiving and 462 on Christmas. New Year’s also had a big change, from 36 in 2010 to 349 in 2019. In general, 2019 was much busier than 2010, with about 1400 outgoing Office Actions per day versus around 800 in 2010.

Office Action Responses also grew over time with each of 2018-2020 seeing between 226 and 255 responses iled on Thanksgiving. Christmas was slower, and New Year’s the slowest of all, with about 2/3 as many responses filed as Christmas or New Year’s. The average number of responses filed per day is much lower than the outgoing documents, and only grew from around 400 per day in 2010 to around 700 per day in 2019.

What did we learn from this? First, Americans are increasingly terrible at taking time off. Part of this is due to the ease of working remotely — something that the Trademark Office has long taken the lead on, but something that has carried over to private practice as well. Second, the Office isn’t too enamored of New Year’s Day. A surprising number of Examiners are deciding to start hitting their quotas for the year right off the bat. Despite it being a holiday, 2020 saw almost 50% of the usual Office Action activity level, and recent years have been north of 20% of normal consistently. No other holiday even approaches that level of activity, although the number of filings on Thanksgiving the last two years got close. International applicants (who don’t have the holiday) are driving a lot of that filing volume, though, so it’s not as focused on US lawyers’ behavior as the Office Action activity.

Have a good one, and, please, take a dang holiday once in a while.

We all know that pumpkin-related products are far more common on the shelves in the autumn. This quick Friday blog looks at the highly important question: how seasonal are filings for pumpkin-related marks?

Not really very seasonal! That’s a bit surprising, because people care about pumpkins a whole lot less outside of the fall. We looked at filing numbers for both marks that contained PUMPKIN and marks with pumpkin in the description of goods, and compared the overall filings from 2010-20 and filings just in September/October/November of those years.

On the mark front, applications for PUMPKIN marks were very slightly more common in the fall, accounting for 32% of applications. Filings with “pumpkin” in the goods, in contrast, was essentially exactly on par with the rest of the year: 25% of total applications.

There are a few things that could be going on here. First, and probably the key factor, is that many companies offer pumpkin-themed products under their house marks or key products marks, from Starbucks coffee to Special K cereal to Kind bars and many more. These include “pumpkin” or “pumpkin spice” in the descriptive text of the packaging, but not in the mark itself, and so don’t necessitate any other filings. Second, companies often plan ahead, and get applications on file well in advance of a product launch. That “spreads out” applications over the year.

As a final check, we did a quicker search of the COLA registry at the Alcohol and Tobacco Tax and Trade Bureau. As common as pumpkin-y craft beers and flavored spirits are, and since seasonal variants often have different packaging that IS registered, we thought a quick search might show real differences. Nope! Only about 21% of COLA registrations that included “pumpkin” as the brand or fanciful name were filed in the fall months.

Like many of our readers, we nodded along in agreement with the TTAB while reading the most recent Monster Energy opposition decision, Monster Energy Co. v. Cavaliers Hockey Holdings, LLC, Opp. No. 91240680 (TTAB Oct. 6, 2020) (hat tip to John Welch for his tireless blogging) . The Board held that the mark CLEVELAND MONSTERS (stylized) for a variety of merchandised goods was unlikely to be confused with MONSTER for energy drinks and various merch; jewelry, clothing, printed materials, and retail services present in both applications.

While the MONSTER mark was conceptually and commercially strong for beverages, the Board found that marks as a whole were quite different, and the teams’ longstanding use as CLEVELAND MONSTERS mark and its predecessor LAKE ERIE MONSTERS mark for the sports franchise. The considerable evidence of third-party registrations including MONSTER carried quite a bit of weight, finding that MONSTER was conceptually weaker and diluted for other products and services.

This got us thinking about how we’d use TM TKO’s tools to pull together this sort of evidence for a Board proceeding.

First, let’s pull evidence that MONSTER is diluted. The easiest way is a manual search of MONSTER marks by class (14 first, then 25, etc.; sort the results by owner, flag the key ones, and export a summary to Word format and export the TSDR status and title copies for the exhibit using the TSDR export button. Class 14 alone has 8 different owners other than Monster Energy with co-existing marks that included variations of MONSTER as a term. You would then repeat for each class that was at issue.

(You could also pull dilution evidence with a ThorCheck Term Coexistence search, looking for MONSTER in both marks and checking the “include non-exclusive term matches” box. This generates a report showing examples of MONSTER co-existence, with the most similar marks sorted in each class, and the report overall ordered by class.)

Second, let’s pull evidence that adding a term like CLEVELAND is enough to avoid confusion. We can use a ThorCheck Term Difference search, adding CLEVELAND as the term by which two otherwise-similar marks differ. Looking at the relevant classes, we see the CLEVELAND CAVALIERS and VIRGINIA CAVALIERS co-existing in a bunch of classes, plust marks like CLEVELAND AGAINST THE WORLD and DETROIT AGAINST THE WORLD and CLEVELAND BROWNS and BROWNS LONDON in Class 25, CLEVELAND ARMORY vs. THE ARMORY in Class 35, and more. After exporting these results (Word and TSDR), you can repeat for other city names and amass other evidence that consumers are used to a city name + nickname adequately differentiating two marks.

Finally, we can find examples of USPTO Examiners issuing refusals based on the common term MONSTER but letting the junior application through to publication. This obviously isn’t binding on the Board, but it doesn’t hurt to provide examples of other reasoned decisions that reflect your position. A quick manual search of just examples where both the senior and junior marks are still active and the junior mark has been published or registered finds over 100 examples, including more than 30 where the prior cited mark was a single word, as here. If we broaden the search out to those that co-existed at some point in the past but no longer do, we’d certainly find a number of additional examples.

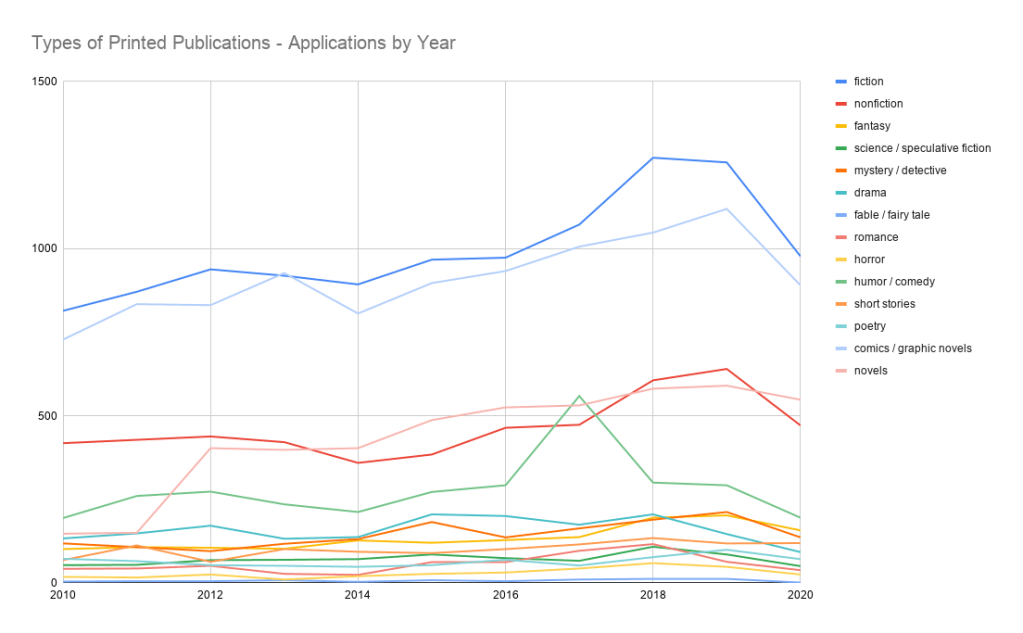

We did some research on the relative commonality of different types of printed fiction over the period 2010-2020, to see if trademark filing trends have varied over the years. Drum roll… they haven’t, really. Filing numbers for types of genre keywords remained incredibly consistent over the years. General terms like “fiction,” “nonfiction,” and “novels” were all extremely popular – no surprise, since the trademark registration process incentivizes applicants to use broad descriptions to claim as much “turf” as possible.

The one big surprise – at least for the author – is how common filings for comics and graphic novels were. It was the single most common specific genre, dwarfing many more traditional categories. To speculate without a whole bunch of concrete evidence, I’d guess that there two things driving this. First, there seem to be more small publishers active in the comics / graphic novels front. Second, more authors in the space may be seeking trademark protection for characters, etc. with an eye towards licensing or merchandising than other genres, given how permeable the membrane between comics and TV/movies have been (at least at the high end). The fact that many comics are sold in a series also makes the registration process simpler compared to novels, where the “single creative work” rule has traditionally made the registration process difficult or unobtainable for authors.

How does this match up with sales figures? Per Book Ad Report, the top fiction genres in order were romance ($1.4b), mystery and sci-fi (between $728m and $590m), then children’s ($160m; not done as a separate category when we ran our numbers) and horror ($79m).

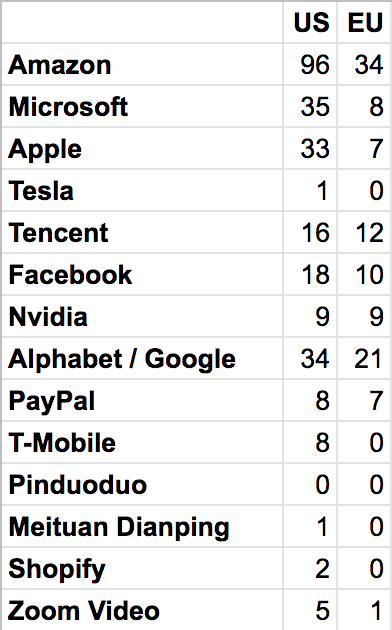

This blog post takes a look at how a few top companies that the Financial Times identified as “prospering in the pandemic” have treated their trademark portfolios during since March 2020. For the purposes of this blog post, we’ll just look at new applications in the US and EU. This will almost certainly under-count the final numbers from the March – September time period, since sophisticated companies tend to use “stealth” filings in out-of-the-way jurisdictions to get applications on file and trigger the Paris Convention priority period, but stay under the radar.

Tech titans Amazon, Microsoft, Google, Facebook, Tencent, Nvidia, and Paypal all had a good number of applications in both the US and the EU. Jurisdiction-specific companies like T-Mobile USA primarily had filings in the US, and Pinduoduo and Meituan Dianping (both mainly active in China) didn’t do much in either market. Tesla, Shopify, and Zoom Video all had fewer filings, but rely largely on their strong house marks more than secondary product-level branding.

These numbers aren’t markedly different from the prior year — a little variation, but nothing more than the usual ebb and flow of product launches would suggest. While these companies have been financially successful in riding out the the pandemic from a profits perspective, they haven’t seen a corresponding boom in trademark filings.

Our big summer project has been a set of data expansion projects. While these aren’t live on the production server yet — although they’re coming soon — this blog post provides a little sneak peek at some research into the sports market in the US and Canada. There aren’t any revolutionary findings here: Canadians are way more into hockey and more into rugby and cricket than Americans, but it was still interesting to see the intuition play itself out in the data.

To test the relative interest in the sports, I looked at active, use-based applications or registrations in Class 28 (sporting goods) or 41 (sporting events or training services) in both jurisdictions. The US search criteria was a bit more restrictive, looking only at a keyword in the targeted class. Canada just looked for both the keyword and the class together, although not necessarily the keyword in the class. That difference resulted in the US and Canada having very similar counts, despite the US obviously being the much larger market and trademark registry.

I also really should have included softball in a combined count with baseball, but forgot, and probably should have thrown lacrosse in too, but this post isn’t going to have enough readership to be worth re-doing the numbers.

Soccer, baseball, golf, tennis were pretty comparable in both countries. Basketball and football were relatively more popular in the US, and, as noted above, hockey, rugby, and cricket were proportionately more popular north of the border.

Compare those filing numbers with the “favorite” and “participation” numbers in the US for the major sports from Wikipedia.

Golf wasn’t included in the Wikipedia table; other sources estimate ~22m participants in the US.

The other thing that stood out is how weird golf is. It has far, far more filings than its relative popularity as a sport would suggest. Presumably part of this is its “gadgety” nature — the sport requires expensive clubs and balls, and lends itself to the use of lots of training accoutrements. To some extent, money can buy (slightly) better results, and the golfing demographic tends to have some cash to spend. In contrast, a sport like basketball really only requires some shoes and a ball, both of those tend to last a while, and a nice new pair of shoes is going to have more aesthetic than functional impact. The continuing (although less dramatic) need for equipment spend probably buoys the tennis and baseball trademark filing numbers a bit, too. Curiously, while football and hockey are pretty equipment-intensive, they don’t see the same spike in trademark filing. These tend to be more “young men’s games,” with participation rates that quickly drop way down compared to viewing interest. As such, while they might be lucrative to present on TV and drive wind on sports radio talk, they don’t generate the same kind of ongoing gear spend that a more lifelong sport does, and that seems to be reflected in the trademark filing trends.