New 2026 Clearance Model! We thrilled to have our new 2026 clearance model live on production.

Setting the benchmark for clearance depth and clarity, you will see improved matching and prioritization of semantic meaning, spelling variations, abbreviations, translations, and more. You’ll get clear results that you can act on quickly, risk indicators, and more responsive watch results.

You also get powerful new filter options to help you slice and dice results to best focus on your key objectives, and industry breakouts of visualizations to help you better segment searches that cover multiple product areas.

Mark Neural Criteria. Simplify and improve custom criteria in field-based searches and watches with one mark field that leverages model-based similarity.

Domain Names. 300+ million records, all enabled for clearance, search, and watch.

Pharmaceuticals and Substances. Our house-mix dataset brings together pharmaceuticals, biologics, natural products, vitamins and dietary supplements, food and cosmetic ingredients, homeopathic substances, and pharmacopoeia references from dozens of sources. Reports include POCA scoring and nomenclature stems. Enabled for clearance, search, and watch.

Demand Letter Drafting. Building on the 2(d) Response Drafting tool, the new Demand Letter Drafting tool helps you quickly move from identifying a relevant result to generating a quality draft demand letter.

Design Common Law Returns. After a hiatus following Microsoft’s end-of-life of the Bing Search APIs, we’ve integrated Google Vision with similar capabilities.

Multi-Factor Authentication. Use your favorite authenticator app for an extra layer of protection for your account. SAML Single Sign-On is available as well for firms with an identity provider.

In Case You Missed It. If you haven’t taken full advantage of other recent enhancements, they include:

“Color” marks are a bit of an oddity for trademark professionals — a color or set of colors applied to a product, packaging, or the means of providing a service that has a source-indicating function rather than a merely decorative importance.

These are difficult to search for, even using advanced AI models — like our new AI search tool! You should try it; it’s awesome!, because the mark can be displayed in several ways that look very different from each other: (1) a color swatch or swatches, (2) a drawing of an object to which the color is applied, shown in color, and (3) a drawing of an object to which the color is applied, but with stippling serving as a “code” for the color, and (4) multiple views of (2) or (3) in a single filing. Furthermore, the various angles and ways the product in (2)-(4) could be displayed could end up looking fairly different but are still representing the same mark.

One significant complication is that the USPTO and most other trademark offices deal with color marks differently, from a data perspective. Many jurisdictions around the world include a data point, which we store in the “Feature Type” field for manual searches, that identifies color marks, sound marks, holograms, smells, etc. While this data coding isn’t perfect, and often has things tagged that actually aren’t true “color” marks, it’s still pretty good and very convenient. And then there’s the UPSTO, which… doesn’t.

Instead of a single, nice, clean variable, the USPTO jams indicators that identify “color” marks into its design coding system. This is actually one of the biggest ways the USPTO design codes differ from the Vienna design code system. In the Vienna system, codes starting with 29 are just color identifiers. The mark is a pig logo that has some pink in it? Great. 29.01.01. In the USPTO, it’s a lot more complicated — the pink in the pig may only show up as a part of the color claim and/or the mark description. Instead, the color-related design codes in section 29 replicate the “color” mark boolean that is much more efficiently conveyed in other jurisdictions. The tradeoff is that the USPTO provides a little more depth, with separate categories for (a) single-color and (b) multi-color marks, (b) used on the entire items or (c) just a part of it, and for those color marks (d) used on products or items used in providing for services and (d) used on packaging or (e) other advertising, and the various combinations of these three sets of values.

So, how do you do this in TM TKO? Let’s pretend that your client is a pharmaceutical manufacturer, and has asked if they can obtain protection for a “color” mark that is a bright yellow pill (or, if not, a yellow stripe on a pill). In the US: https://www.tmtko.com/searches/2938217 for yellow just on product, or https://www.tmtko.com/searches/2938215 for any yellow on products/packaging. Internationally, it’s simpler — something like https://www.tmtko.com/searches/2938219, for a similar yellow in the EU. (And, yes, I picked yellow because it’s relatively less common.)

We are excited to announce our new, machine-learning-driven image clearance tool. Just log in and go here to try it — we’d love to hear from you about your experiences. As with all of TM TKO’s tools, access is included in any subscription or day pass.

The new system is simple. Just drop in an image; you’ll be able to crop it if needed. If you want to add US and/or Vienna design codes (particularly helpful if you have a “busy” image with a lot of visual elements, but you are most interested in one feature in particular), you can do so. Hit search, and you’ll be off.

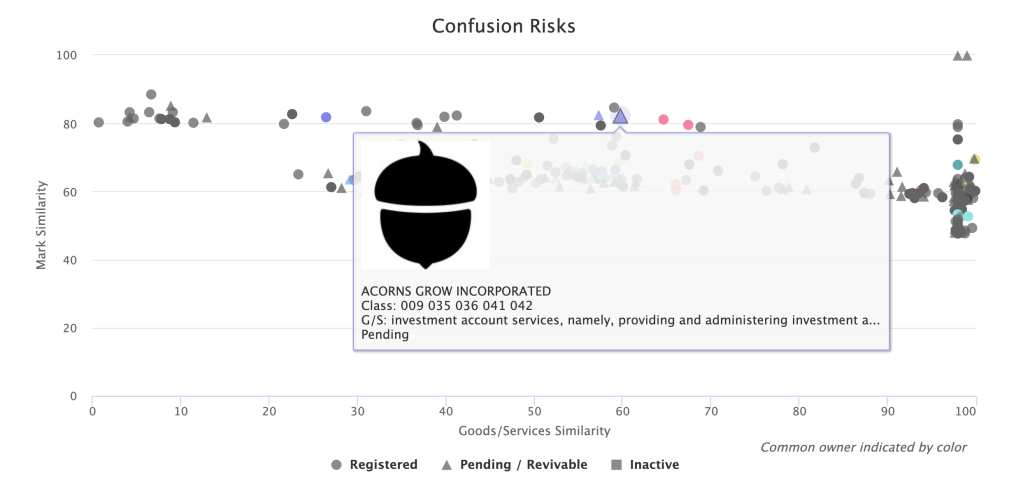

We replicated a search for a recent application for an acorn logo for insurance services here, so you can see it in action. The first two results are the filed-for mark and a co-pending application with the same owner. So far, so good. Another acorn design that was cited by the Examiner was the #4 result, with another, similar acorn in between.

As with TM TKO’s other clearance tools, your search report includes helpful visualizations of mark and goods similarity, helping you quickly triage risks and get an answer to your client both quickly and accurately.

If you choose to include common-law results, you will get an additional section of image results sourced from Bing.

We have been working on this for quite a while, and are very happy to have this out in the world for you to use! Watches and portfolio-driven watches will be available soon.

This type of quick post might become a semi-regular feature, but, for now, consider it a one-off. Looking at a few recent Office Actions today, one caught my eye – a Madrid-based application into the US for the mark MOFFAT, for a variety of cooking equipment.

The Office raised a couple of issues in the Office Action of March 13, 2024 – weirdly, listing some but not all of them in the “Summary of Issues” section. The two of interest were a 2(e)(4) refusal (primarily merely a surname) and a 2(d) refusal (likelihood of confusion with a prior registration for MUAFOT for similar goods).

These two refusals seemed inconsistent to me. If MOFFAT is primarily merely a surname (and “Moffat” is certainly, at the least, often a surname), then it will be viewed as a unit as that name. MUAFOT differs only by some vowels and a repeated consonant, so it’s going to hit on phonetic searching algorithms, but I think an actual human viewer parses these quite differently — the pair “UA” isn’t even really a diphthong in English, so a viewer would likely pronounce each vowel separately. However it’s parsed, I think, it’s not likely to be understood as “a variant of MUAFOT.”

Are other applicants making similar arguments? Yes! Applicants have made comparable arguments to distinguish marks like, say, EMME and EMMA, FOLI and FOLEY’S, WOLFF vs WOLF, KROM vs CHROME, CIVELLO vs CHEVILLOT, and etc., and some poking around in TM TKO can find similar examples of those two issues paired in refusals where the applications subsequently made it through to registration.

You have reviewed a search report, starred the results you want to talk with your client about, exported a chart to attach to an email — and now you have to actually put fingers to keys and draft the damn thing. Ugh.

Now, you can skip this minor moment of despair! TM TKO has added a new “Analysis” button that will create a smart, contextually-sensitive draft analysis for you.

Let’s say you have run a search for the mark OUTLAW BUGS, to be used with insecticides. You flag a handful of registrations with the appropriate risk levels (red = high; yellow = moderate; green = low), each of which contains the shared term OUTLAW. Then, you hit the “Analysis” button. In a few seconds, TM TKO generates a draft for you, such as the following:

We analyzed a search for the mark OUTLAW BUGS (the “Searched Mark”) for insecticides in class 005 (the “Searched Goods”).

The trademark OUTLAW owned by SERGEANT’S PET CARE PRODUCTS, LLC presents a high risk of confusion with the Searched Mark OUTLAW BUGS. The mark OUTLAW is identical to the Strongest Word in the Searched Mark, which significantly increases the likelihood of confusion. Additionally, the Searched Goods “insecticides” are closely related to the goods “insect repellent for companion animals, namely, horses” associated with the OUTLAW mark. Both products are used for pest control and could be found in similar retail environments, which could lead consumers to believe that the goods come from the same source.

HELENA HOLDING COMPANY’s trademark OUTLAW poses a moderate risk of confusion with the Searched Mark OUTLAW BUGS. The mark OUTLAW is again identical to the Strongest Word in the Searched Mark, which is a significant factor in the analysis of potential confusion. However, the goods associated with this mark, “herbicides for commercial, industrial and agricultural use,” while in the same class, are not as closely related to “insecticides” as insect repellents are. Herbicides target plants rather than insects, which may reduce the likelihood of confusion among consumers, but the similarity in the marks and the overlap in commercial channels where these goods may be sold still contribute to a moderate risk.

The OUTLAW FEED mark owned by DBA Outlaw Nutrition, Outlaw Feed, LLC carries a low risk of confusion with the Searched Mark OUTLAW BUGS. Although the mark contains the word “OUTLAW,” the addition of the word “FEED” differentiates it from the Searched Mark. Furthermore, the goods “animal feed supplements” are not similar to “insecticides,” as they serve entirely different purposes. This difference in the nature of the goods greatly reduces the risk of confusion.

This is a quick and easy way to blast right through writer’s block and have a serviceable draft ready for your fine-tuning. You work more efficiently, and, particularly if you’re working on a fixed fee, more profitably.

How does it work? We use generative AI (under terms of service that protect confidentiality and prohibit any use of the data included for further training by the AI model) together with tightly controlled business logic to give you smart, tailored analysis nearly instantly. Of course, like any work product, you’re ultimately responsible for making sure that the final product reflects your analysis — but this gives you a big step up in doing good, efficient work.

TM TKO now includes TTAB data! Just like with our Office Action research tools, thoroughness is the key – you aren’t just limited to final decisions. You can search through decisions, rulings, pleadings, motions, and more to hone in on strategies and arguments that have worked for others in situations similar to the one your client faces. You can now do vastly more complex research than the TTAB’s Reading Room decision-only search options allow.

TTAB proceeding research

Track down proceedings that fit a fact pattern. It’s simple to find oppositions or cancellation actions where both parties’ marks include the term GREEN, or to find where a senior party making soda opposes an application for beer (representative sample shown below), or to identify strategic patterns in highly litigious counterparties.

TTAB document research

Find specific models to assist your drafting process and meet your needs. You can be done with adapting general model documents — it is now simple to find prior motions or briefs that address your key issue with TM TKO. You can do better, more efficient work.

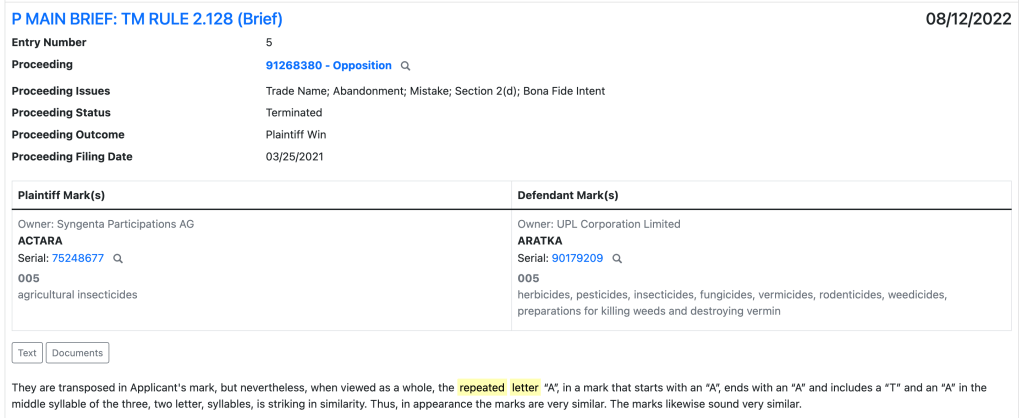

For example, if you’re searching for arguments about a “repeated letter,” you can track down similar arguments in seconds.

Appeal research

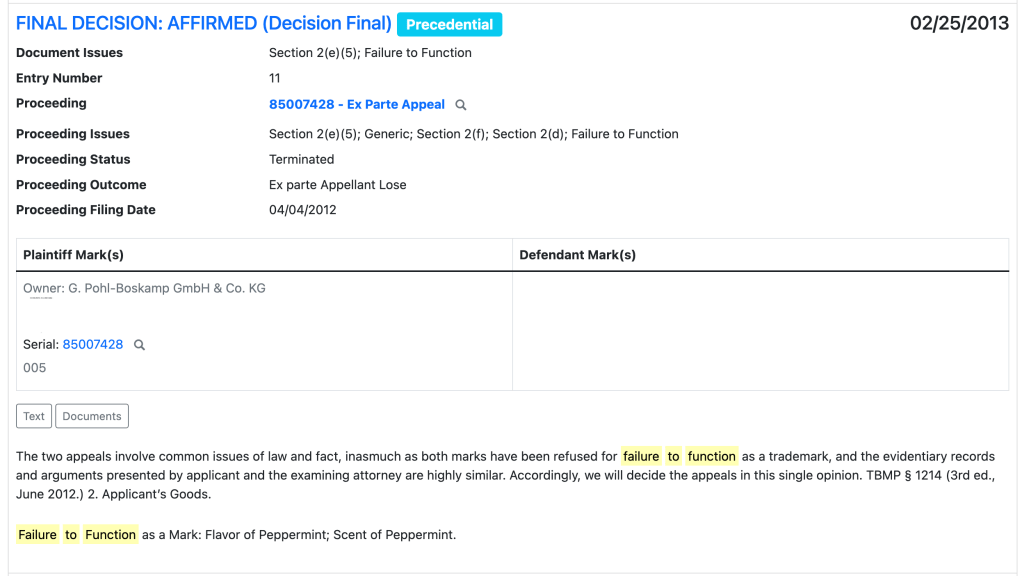

Find briefs that have been effective on your specific issue, or free-text search to find how other lawyers are effectively citing to a specific case or building a particular style of argument. For example, you can search for appeal decisions relating to “failure to function” refusals, and then sort by precedential decisions.

Clearance

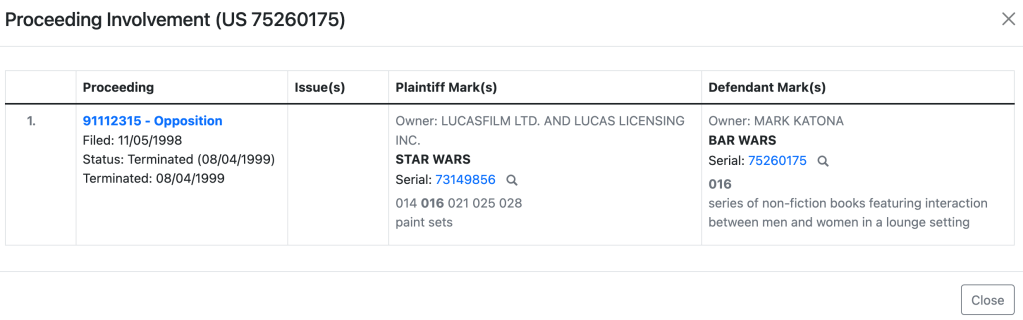

Clearance reports now embed valuable opposition, cancellation, and appeal data. You can now identify aggressive potential opposers without further research. Where applicable, you will see a “Proceedings” line in the Mark field of your manual or automated search results, as below.

Click in to quickly see more details about the proceeding in question via a popup. If you need to dig further, just click on the link to the proceeding number to go to the full details page.

Get researching!

Try it today! We’d love to hear what you think, and when you have been able to make use of the new TTAB research tools to improve your client outcomes. And, of course, make sure to mention this to your litigation-focused colleagues who may not have used TM TKO before.

As a trademark practitioner, you know that not all Office Actions are created equal. If your Office Action just raises an issue with a specimen or a disclaimer request, there may be some back-and-forth with your examining attorney, but the issue will almost certainly get resolved sooner or later. You can get a feel for how likely an issue is to be resolved prior to publication with our Office Action analysis tool and the Examiner analytics it provides.

If, however, you run into a functionality refusal or a likelihood of confusion refusal, you’re likely looking at at least one round of substantive back-and-forth. Applications running into these sorts of refusals move forward to publication at a much lower rate, as we’ve detailed in some prior blog posts.

What sort of refusals, then, did the USPTO tend to issue in 2022? The big ones were:

Substantive Refusals

Likelihood of Confusion

23%

Descriptiveness

18%

Non-Substantive Refusals

Specimen

30%

Classification

25%

Disclaimer

22%

Mark description

14%

Domicile

12%

All numbers are a percentage of times an issue was raised in any Office Action in 2022. Many Office Actions contain multiple issues, so these percentages will not add up to 100%.

Foreign registration-related suspensions and applicant entity clarification requests were present in around 4% of Office Actions each. No other issue exceeded 2% frequency.

A few interesting points arise from this data, particularly the large numbers of non-substantive refusals.

The Office Should Change the Process for Assigning Mark Descriptions. Mark description issues are far more common than I expected. It might be more efficient for the Office to simply assign mark descriptions and allow applicants to object, similar to the process for design codes. That process is highly effective, and applicants rarely push back on the Office’s preferred design coding (or, indeed, the description of the mark phrasing). The change of process would permit some otherwise perfectly acceptable applications from either going abandoned for lack of a response, and speed examination time for almost all of the rest.

Classification Issues Aren’t Going Away. The heavy incentives towards TEAS Plus filing are not enough to eliminate identification woes. While the Office’s ever-widening price gap between TEAS and TEAS Plus is an attempt to mitigate this issue, it can’t solve the whole problem — indeed, it will never solve the issue for any Madrid-based applications. Only further efforts to create a worldwide equivalent of the ID Manual would not only help speed up prosecution in the US, but could address the maddening inconsistencies between what constitutes an acceptable definition goods in various countries. If WIPO could incentivize (e.g. through filing fees) use of such “universally accepted” language, it would be a big improvement for the international trademark system.

Disclaimer Practice is a Drag. Disclaimer requests are really, really common, popping up in over a fifth of Office Actions. Disclaimer practice in the US is riven with inconsistencies; the same term showing up in a short mark will get a disclaimer request; if the mark has a pun in it or if the term is used in a tagline that’s barely any longer, it’ll avoid a disclaimer request. It’s all very silly.

There has to be a better way. A simple, hard-and-fast rule would remove much of this back-and-forth. For example, the Office could adopt a rule that a term that is used in active registrations more than X times (3? 5?) by different owners in a single class is presumptively not likely to cause confusion with another mark, unless there is other evidence of mark similarity like other terms in the mark, visual presentation, etc. That would have two big benefits. First, it would dramatically simplify the confusion analysis. (As a side effect, it would stop the Office from issuing the annoying refusals where 6 companies own registrations for TERMX + SECOND TERM, someone slips through a registration for TERMX alone for narrow goods, and then every subsequent applicant for TERMX + SECOND TERM style marks gets a 2(d) refusal that they have to fight about.) Second, it would obviate the need for disclaimer practice. Just count!

As with mark description issues, some otherwise perfectly fine applications are either going abandoned over disclaimer requests, or have to deal with extra attorney fees to reply (and increased total prosecution time). Neither are a good outcome, and the Office should consider a wholesale revamp of the disclaimer practice to fix it.

Conclusion. Hopefully, we’ve not only given you some insight on the types of issues applicants are running into most often, but also provided some interesting ideas about how the Office could revamp its existing processes to better avoid unnecessary prosecution problems.

With 2022 concluded, we’re taking a look back at how the USPTO performed in terms of its throughput, and examination trends in the types of refusals it has issued over time.

I. Trademark Office Examination — Volume and Throughput

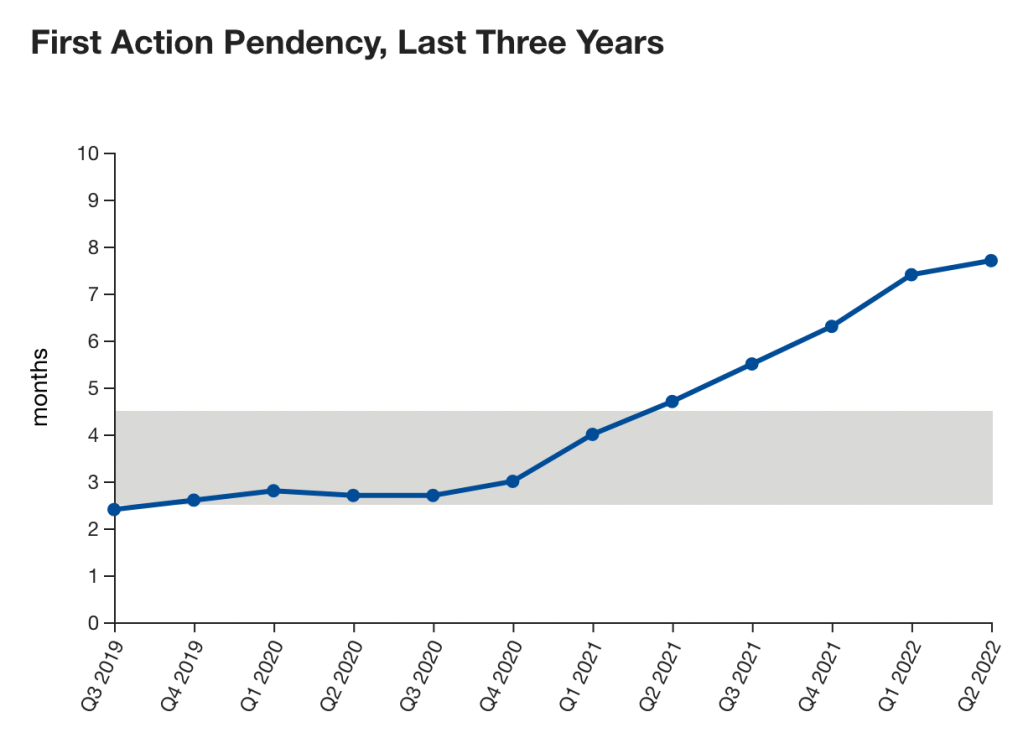

Let’s look at sheer volume — how is the USPTO keeping up? Not well! Per the USPTO’s own data in the Trademarks Data Q1 2023 snapshot, first actions are taking in excess of 8.4 months and total pendency has exceeded 14.3 months.

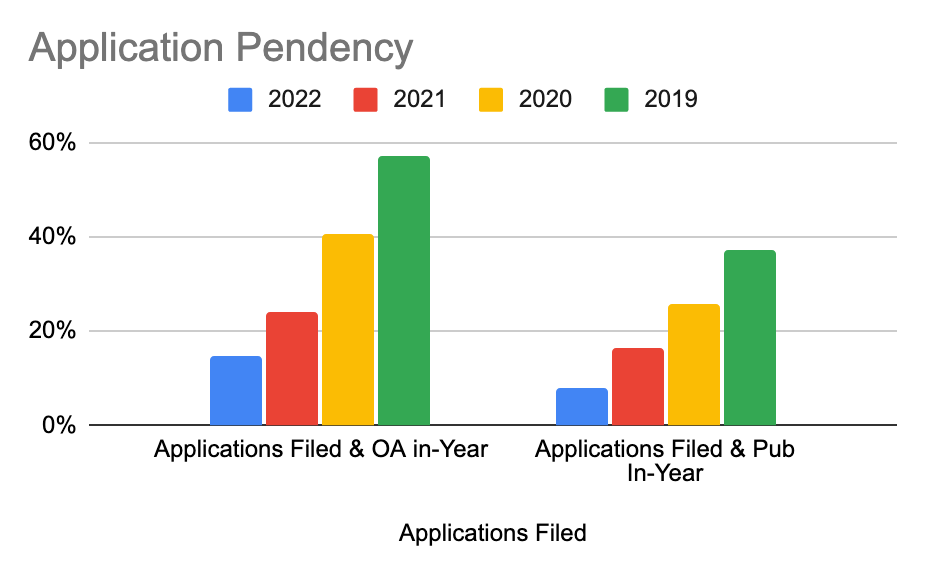

We took a slightly different approach to see how the Office is coping — two approaches, in fact. Overall, application volume was down — in 2020 and 2021, applications exceeded 660,000; in 2022, those dropped a bit to just shy of 550,000. Filing rates remain above the 500,000 filings from 2019. A slowing economy and inflation probably contributed to the drop.

Despite this, the Office is slipping further and further behind. Rates for two indicators of “quick examination” both plummeted — applications that were (a) both filed and given an Office Action in the same calendar year and (b) both filed and published in the same calendar year. Very, very few applications were dealt with quickly in 2022.

II. Refusal Breakdown – What is Blocking Applications in 2022?

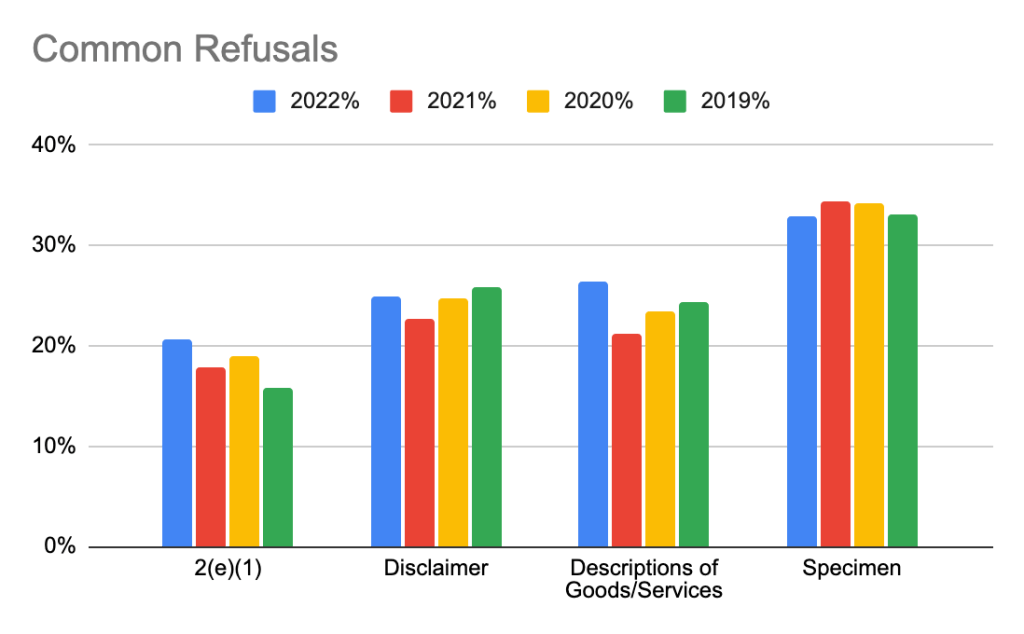

We also took a look at what sorts of issues applications were running into over the same 2019-2022 time frame. First, we examined the most common refusals: likelihood of confusion refusals, descriptiveness/disclaimer requests, description of goods and services changes, and specimen refusals. Each of those issues impact an average of 15%+ of applications examined each calendar year. Acquired distinctiveness-related refusals account for around 6% annually, and messed up the scale of either chart, so it’s been left off entirely.

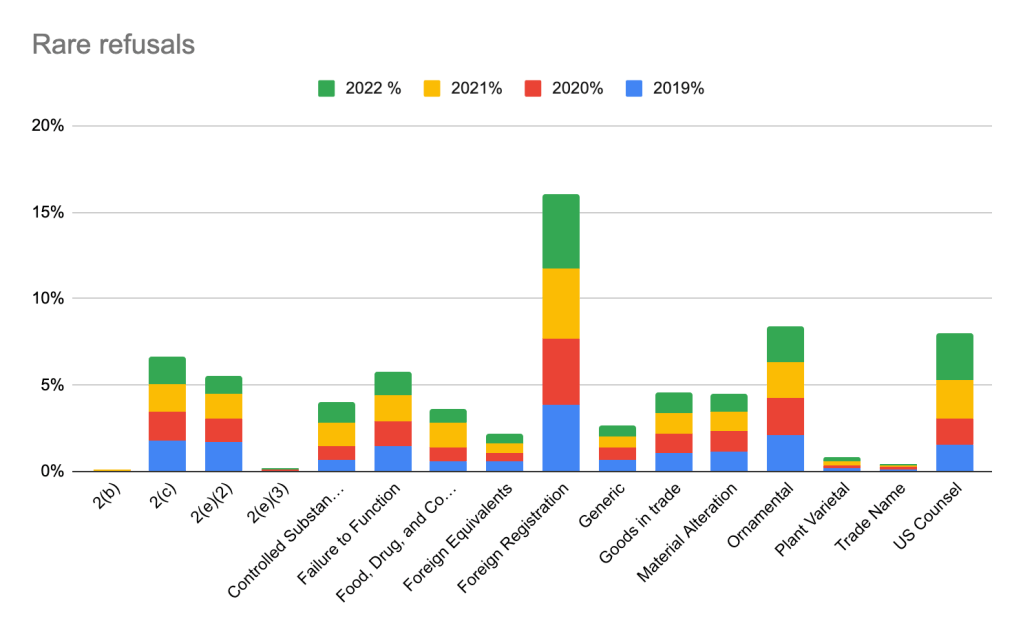

All of the rest of refusals together are a comparative pittance. Some of these refusals are highly clustered — the weed-related CSA and FDA refusals in the cosmetic/pharma/edible classes, ornamental refusals in clothing, etc., and almost never occur outside of those core classes. Others, like suspensions while waiting for foreign registrations to issue, are as evenly dispersed as applications generally.

IV. A Detailed Look at 2(d) Refusals

Between 50% and 60% of 2(d) refusals each year cite to a single prior filing as the cause of the refusal, with about 20-25% each of 2 or 3+ citations. In 2022, more than 40% of the refusals predicated on a single mark had a direct class overlap. Between these, it suggests that a large number of 2(d) refusals are pretty straightforward.

IV. Doing Better – How the Office Can Change

What can the Office do to help reduce its work backlog? Better tools on the front end of the application process might go a long way in ensuring that the Office has less that it needs to examine.

Automated screening of descriptions of goods and services to show applicants (particularly those self-filed or less familiar with the Office process) where the IDs are likely falling short of the acceptable standards would go a long way to addressing an extremely common cause for refusals. Similarly, automatically suggesting disclaimers for terms that are very often disclaimed for the filed-for goods could avoid a lot of the Office Actions around that issue. Finally, some basic screening of identical-mark / identical-class filings would remove a lot of “low-hanging fruit” from getting 2(d) refusals by pushing those applicants to an alternative mark that isn’t immediately and obviously non-viable.

We don’t especially expect any of this to happen, and we are not seeing many promising signs that the Office is likely to catch back up and return to the 3-4 month examination window that most trademark professionals had grown accustomed to.

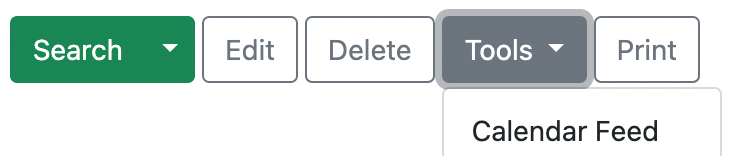

You can now integrate TM TKO’s new Deadlines feature with your preferred calendar. Go to a Portfolio that includes Deadline tracking, and go to the Deadlines tab. Then, in the upper-right corner, select Tools -> Calendar Feed.

On the next page, click “Start Publication.” You will get a secret address URL to your Calendar in the standard iCal format.

Calendar applications generally include the capability to subscribe to a calendar published in the iCal format with a secret address URL. Documentation for adding this iCal link to several common calendars follows:

Apple Calendar See section titled “Subscribe to a calendar”

Google Calendar See section titled “Use a link to add a public calendar”

TM TKO is excited to announce a major expansion of the functionality of its Portfolios feature. Now, in addition to built-in conflict checking and automated watch setup, all Portfolios have a “Deadline” tab. It tracks and automatically generates deadlines for more than 4,000 prosecution events, and automatically shows the next upcoming prosecution deadlines for filings in the Portfolio in any of the jurisdictions where TM TKO offers coverage: US, Canada, Mexico, Australia, New Zealand, European Union IPO, France, Germany, Spain, the UK, and WIPO. Individual trademark records now also have a detailed history of past and future deadlines.

Setting up a Portfolio takes under a minute – just go to the Portfolio page. For instructions, go to the Portfolio help page or see our more detailed blog post.

Never forget a deadline with automatic updates

Attorney Portfolios that include deadline watching – a simple checkbox on your Portfolio setup page – will include automatic weekly update emails. While you sip your Monday morning coffee, go through short, actionable lists:

– deadlines due within the next period; – deadline periods that opened in the last period; and – deadlines that closed in the last period.

Or, hop on the TM TKO platform and view the Deadline tab for that Portfolio to get a broader horizon of upcoming deadlines. It’s simpler than ever to keep track of what you need to be doing to stay on top of your practice.

What’s the cost?

Deadline tracking via Portfolios is included in your TM TKO subscription. There is no change in price, just an increase in functionality.

Bulk Knockout Search – Now Included at No Extra Charge

Bulk Knockout Search is now included for all subscribers with no additional charge. Bulk search lets you quickly input details for a large number of searches at once, and gives you a convenient summary report “on top” of your individual search reports. It’s a super-efficient way to run and review large numbers of reports for a brainstorming client, to effectively manage a large, catalog-type clearance project, and more.

What’s coming next?

TM TKO has many projects underway already. In 2023, TM TKO will expand the new deadline-related features, incorporate TTAB data, expand our international coverage for both search and deadline purposes, continue to advance search, and so much more. We’re looking forward to 2023 being our best year yet.

This blog post expands on TM TKO’s new Deadline tracking feature, and provides more detail about how to set up a Portfolio to get the most coverage.

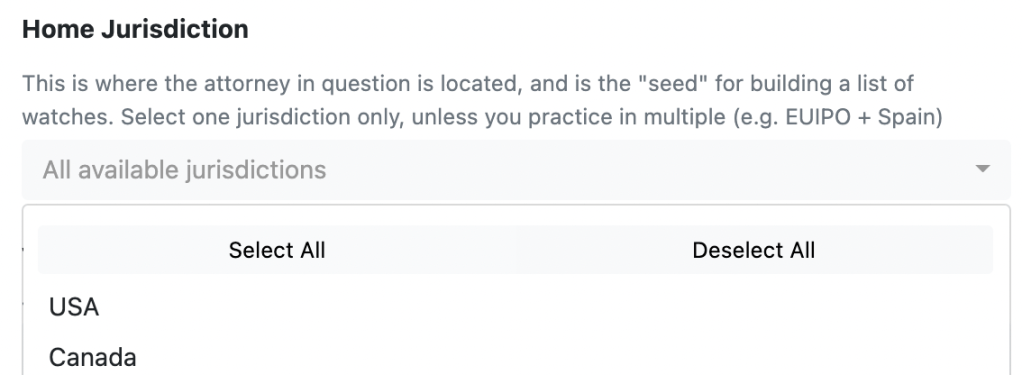

Most TM TKO subscribers use Portfolios as a convenient way to set up watches for a large number of marks at one time. In the US, this is usually done using the correspondent e-mail address; in other countries, attorney or firm name are most common.

When it comes to watching, a streamlined Portfolio is the best. You want to pick a country, usually your “home” jurisdiction, as the base for all your watches — there is no point in having 6 watches for the mark XYZ, all for the same services, just because it’s registered in 6 jurisdictions.

But, Portfolios are very flexible — any search strategy can define a Portfolio. Firms that do dispute-related work for clients that have in-house counsel will often set up a Portfolio for that client based on the Owner name field.

When it comes to deadline tracking, though, you want a comprehensive Portfolio. If your work is all in one jurisdiction, you are already done — the same Portfolio for watch will work perfectly. The “Watch deadlines” option will already be turned on for you. If you’re doing international work as well, you will want a couple of additional steps. The best bet is to set up a supplementary Portfolio to just do deadline tracking.

First, at the top of the setup page, change the Home Jurisdiction to everything — hit “Select All.”

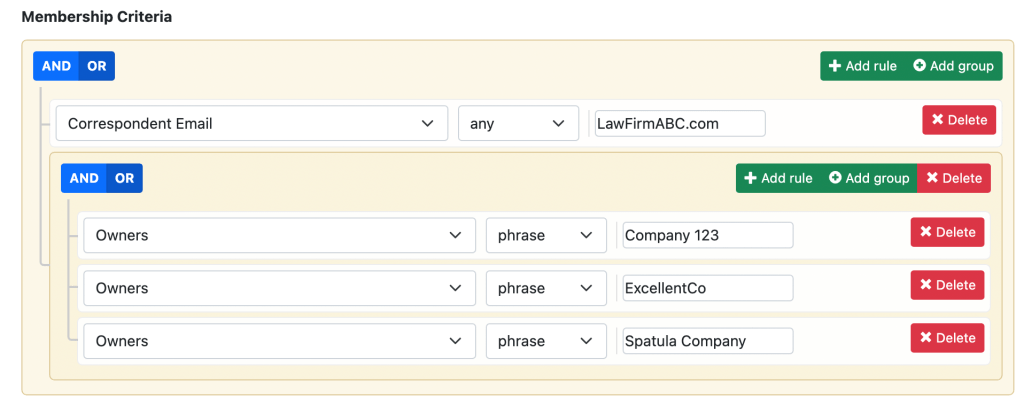

Second, at the bottom of the setup page, make sure to turn off “Watch Similarity” on this Portfolio, to make sure you don’t get a bunch of duplicate watches.

Finally, you’ll want to use two approaches to setting the membership criteria: (a) set up your usual identifier (email/firm/name) in one field, connected by an OR to (b) a group (via “add group”) where you set up a set of Owner fields with “phrase” matching, also connected by an OR. So you’ll end up with something like this:

As you need to add extra companies for international coverage, just Edit this Portfolio — “Add Rule” in the company group and add the new name.

If you have any questions or need a hand in setting up Portfolios to maximize your Deadline tracking, don’t hesitate to email us or set up a time for a web meeting from inside the platform — we are always happy to help.

The USPTO is currently examining new applications at a much slower clip than their historical norm. Rather than expected initial examination within about 3 months of filing, now, by the Office’s own data, it’s at least 7.5 months. That time is probably overly optimistic, since a new application filed today faces an extra 7.5 months of backlog between it and first examination.

The Paris Convention provides US applicants 6 months in which to file internationally and claim the benefit of their US application, and this ends up being a de facto filing deadline for many applications filed via the Madrid Protocol. Applications filed through the Madrid Protocol provide substantial benefits to applicants, including comparatively cheap filings and convenient renewals and assignments. However, registrations issued via Madrid are dependent on the registrant’s home country application(s) or registration(s) for 5 years.

As we know, clients do not always select marks with completely clear paths towards registration. Since it’s now taking way longer for applications to receive an initial examination than the 6 months provided by the Paris Convention, what’s an applicant to do? File via Madrid with some uncertainty? File direct in-country applications?

The USPTO does have a mechanism to accelerate examination. A Petition to Make Special costs $250; if granted, it moves an application to the front of the line for examination. Per TMEP § 1710 – 1711:

A petition to make “special” must be accompanied by: (1) the fee required by 37 C.F.R. §2.6; (2) an explanation of why special action is requested; and (3) a statement of facts that shows that special action is justified. The statement of facts should be supported by an affidavit or declaration under 37 C.F.R. §2.20.

Invoking supervisory authority under 37 C.F.R. §2.146 to make an application “special” is an extraordinary remedy that is granted only when very special circumstances exist, such as a demonstrable possibility of the loss of substantial rights. A petition to make “special” is denied when the circumstances would apply equally to a large number of other applicants.

The most common reasons for granting petitions to make “special” are the existence of actual or threatened infringement, pending litigation, or the need for a registration as a basis for securing a foreign registration.

The Office provides minimal guidance on when Petitions will be refused.

The fact that the applicant is about to embark on an advertising campaign is not considered a circumstance that justifies advancement of an application out of the normal order of examination, because this situation applies to a substantial number of applicants.

The “need for a registration as a basis for securing a foreign registration” is close, but it’s not quite what we need here. You technically don’t need a US registration to survive the Madrid pendency period, provided that you can stall out an application at the USPTO long enough. What we want the quick US examination for is really certainty.

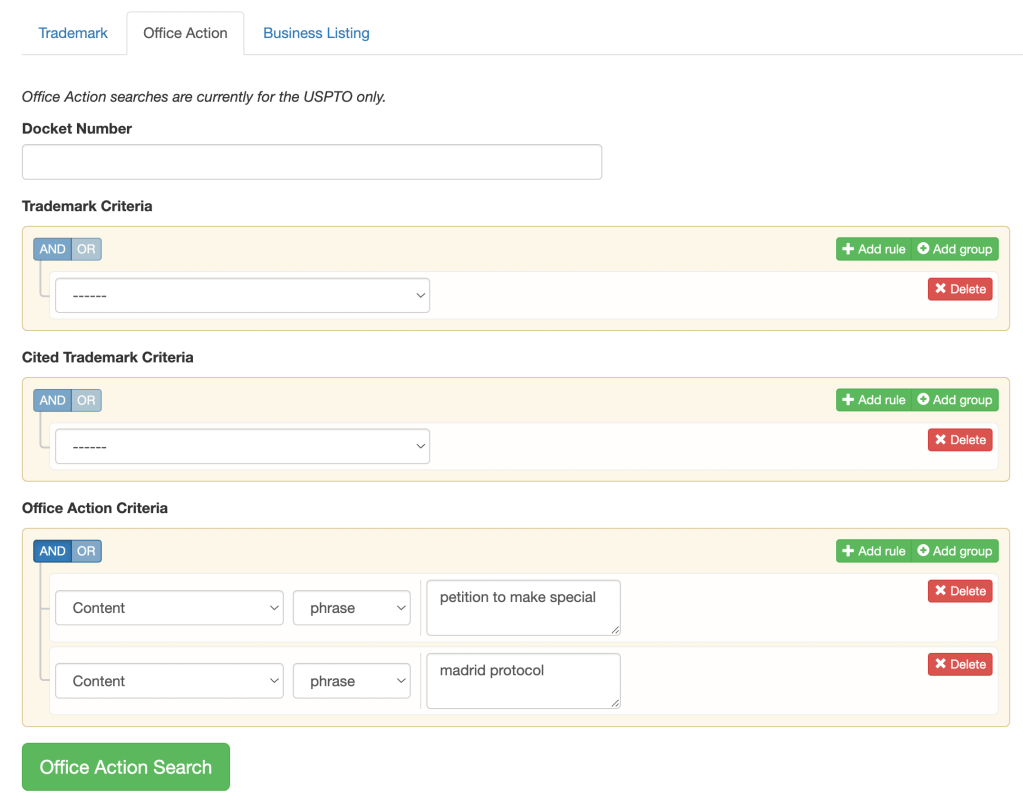

Seeing how these requests turn out is a perfect job for TM TKO’s prosecution research tools. Go to Search and then Office Action, and we can look for documents that have both the phrases “Petition to Make Special” and “Madrid Protocol.”

This finds more than 75 documents. Some of these relate to Petition attachments that use relevant keywords, so we then tweak the search to screen those out, and end up with about 65.

Petition Decision Year

Granted*

Denied

2015

3

0

2016

7

0

2017

6

0

2018

7

0

2019

2

0

2020

8

0

2021

8

5

2022

–

–

*If the Petition was specifically granted or was just examined really quickly thereafter, I counted it as “granted.”

What’s up with the refusals in 2021? These start in July 2021, and the refusals all have some variation of the following:

Petitioner states within the application the need to secure a foreign registration for the above mark. Petitioner omitted the required supporting evidence, e.g., proof showing that a foreign intellectual property office requires a U.S. trademark registration in order to submit a trademark application in that country (…) from the petition.

This is fairly wild. None of the prior petitions from 2015 – 2021 had any evidence whatsoever, and some of these were filed by the exact same attorney using the same request text that had been granted before, and granted dozens of times. It’s dumb that a Petitioner would need to provide — what, a copy of an excerpt of the Madrid Protocol text?? — to the Office for the Office to recognize that the Protocol requires a home country app/reg for the dependency, since the USPTO’s own rules enforce that exact same requirement. Nevertheless, that’s apparently exactly what applicants out to do going forward.